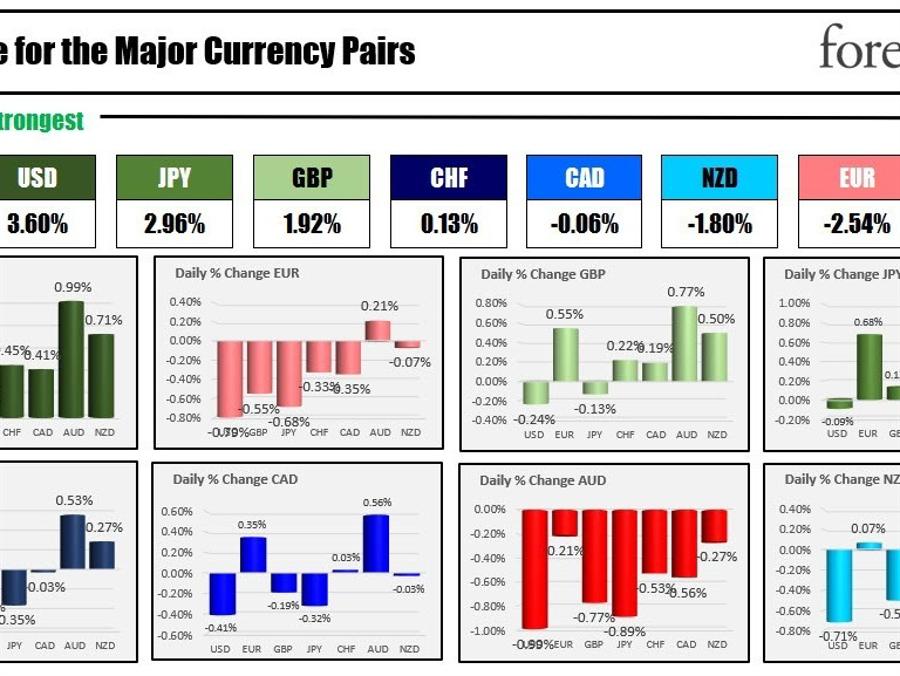

The USD is the strongest and the AUD is the weakest as the NA session begins. Federal Reserve Chairman Jerome Powell reaffirmed his stance on impending rate hikes for the remainder of the year, following a two-day semi-annual Congressional testimony which concluded yesterday. Powell emphasized the necessity of further hikes to combat inflation and meet the central bank's 2% target rate. The likely pace of these increases is also factored in, ensuring the ability to accommodate new data. This stance appears to be widely supported by the Federal Open Market Committee. Traders currently anticipate a 75% probability of the next hike occurring in July, with an additional quarter-point rise later in the year. Although Bostic and Goolsbee were a bit more open to a further pause, the balance of officials seems to be on the Chairman's page. The markets will monitor the comments (and the data) as rates are still data-dependent, with services inflation remaining the key barometer.In the Asian Pacific session today, the flash PMI data out of Australia and Japan were mixed to lower.

Starting with Australia, the manufacturing sector experienced a contraction, with a PMI reading of 48.6. This is a slight improvement over the prior month's 48.4, but it still falls under the 50-mark threshold, indicating an ongoing contraction. Australia's services sector remains in the expansionary territory but just barely with the services PMI of 50.7. That was at a slower pace than the prior month's 52.1 and the lowest level since March. The AUDUSD tumbled lower today with the 100-day MA at 0.67134 being broken to the downside in the process. The pair is testingitss 50% midpoint of the move up from the May 31 low at 0.66785 to start the NA session.

The Japanese manufacturing sector indicated a near-stagnant condition with a PMI of 49.8, falling below both the expected 50.2 and the prior month's 50.6, suggesting a slight contraction. The National Core Consumer Price Index (CPI) year-on-year increased by 3.2%, slightly surpassing expectations of 3.1% but falling short of the previous month's 3.4%. The BOJ keeps the stimulus flowing in Japan despite the elevated inflation.

The EUR has been weak today with today's Purchasing Managers Index (PMI) data releases from Europe showing signs of economic deceleration, particularly in the manufacturing sector. The French manufacturing sector displayed a modest improvement with a PMI of 45.5, slightly higher than the expected 45.4, but lower than the previous month's 45.7, signaling ongoing contraction. More concerning was the notable dip in the French services sector with a PMI of 48.0, significantly falling short of the anticipated 52.2 and marking a decline from the previous month's 52.5.

The data from Germany mirrored the French downturn, with the manufacturing PMI of 41.0, which was lower than both the anticipated 43.6 and last month's 43.2, suggesting a deepening contraction. While the services sector remained in expansion territory with a PMI of 54.1, it was less robust than the forecasted 56.3 and the previous month's 57.2.

The overall Eurozone figures reflected these trends, with a manufacturing PMI of 43.6, which was below the expected 44.8 and equivalent to last month's reading. The services PMI came in at 52.4, showing continued expansion but at a slower pace than the forecasted 54.4 and the prior month's 55.1.

In the UK, the manufacturing PMI of 46.2 also indicated a contraction deeper than the expected 46.9 and the previous month's 47.1. The services sector maintained growth with a PMI of 53.7, but this was less than the predicted 54.8 and last month's 55.2. Also, released in the UK, retail sales grew by 0.3% month-on-month, exceeding the forecasted contraction of 0.2%. However, the growth was slower than the prior month's increase of 0.5%.

In summary, the PMI data suggests that while the service sectors continue to grow in Europe, they are doing so at a slower pace than expected. Meanwhile, the manufacturing sectors across the region are continuing to contract, hinting toward a broader slowdown in economic activity.

US stocks are lower in premarket trading. The major indices are on track to close lower for the week. That would snap the S&P string of 5 consecutive weeks with higher closes, while the NASDAQ index is on track to snap its 8-week win streak. US yields are lower despite the USD rise (flight to safety flows are dominant today). Oil is down and on pace for the biggest decline since May 1 week.

A snapshot of the markets currently shows:

* Crude oil is trading down -$0.80 or -1.15% at $68.70. The price of crude oil is down -4.49% this week on concerns about global growth as central banks hike rates

* Spot gold is trading up $6 or 0.32% $1990.40. Lower yields are helping to support the price along with technical support at the natural support level at $1900. The low price today reached $1910.26.

* Silver is up $0.14 at $22.35

* Bitcoin is trading steady at $30,140. The level near 5 PM yesterday was trading right around the $30,000 level

In the premarket for US stocks, the major indices are trading lower in premarket trading

* Dow Industrial Average is trading down down -114.71 points after yesterday's -4.81 point decline. The index is on pace to snap a 3-week up streak

* S&P index is trading down -22 points after yesterday's 16.22 point rise. The S&P is on pace to snap its five-week up streak.

* NASDAQ index is trading down -95 points after yesterday's 128.41 point rise. The NASDAQ is on track for its worst week since April 6.

In the European equity markets, the major indices are all trading lower

* German DAX down -0.87%

* France's CAC down -0.35%

* UK's FTSE 100 down -0.36%

* Spain's Ibex down -0.74%

* Italy's FTSE MIB down -0.32% (delayed)

In the Asian Pacific market today, Japan and Australia is indices fell. China was closed for holiday:

* Japan's Nikkei fell -1.45%

* Australia's S&P/ASX 200 index fell -1.32%

In the US debt market yields are lower

* 2-year yield 4.745% -5.5 basis points

* 5-year yield 3.982% -6.2 basis points

* 10-year yield 3.736% -6.2 basis points

* 30-year yield 3.825% -4.8 basis points

In the European debt market, benchmark 10-year yields are sharply lower as concerns about growth and too tight policy weigh on yields.

This article was written by Greg Michalowski at www.forexlive.com.

http://dlvr.it/Sr8nZ6

Comments

Post a Comment